How to Calculate Monthly Mortgage Payments. Understanding how to calculate your monthly mortgage payment is one of the most practically valuable financial skills a prospective homebuyer, current homeowner, or real estate investor can possess. Your monthly mortgage payment is not simply a number your lender assigns you — it is the direct mathematical result of your loan amount, your interest rate, your loan term, and a set of additional cost components that significantly affect your true monthly housing obligation. Understanding exactly how that number is derived puts you in complete control of your home financing decisions.

The difference between a borrower who understands their mortgage payment calculation and one who simply accepts whatever number appears on their Loan Estimate is the difference between a borrower who can negotiate intelligently, compare lenders accurately, evaluate refinancing opportunities with precision, and plan their household budget with genuine confidence — and one who is entirely dependent on lenders and loan officers to interpret their own financial situation for them.

This comprehensive guide walks through every component of the monthly mortgage payment calculation — from the core mathematical formula to the additional cost layers that constitute your true total housing payment — alongside practical tools, real-world examples, and the financial planning strategies that help you manage your mortgage cost intelligently over the life of your loan.

The Four Core Components of a Monthly Mortgage Payment

Before calculating your monthly payment, you need to understand that what most people refer to as their “mortgage payment” is actually composed of multiple distinct elements. These are commonly abbreviated as PITI — Principal, Interest, Taxes, and Insurance — with a fifth element, Private Mortgage Insurance or PMI, added for loans where the down payment is less than 20%.

Principal is the portion of your payment that reduces your outstanding loan balance. In the early years of a mortgage, principal represents a relatively small fraction of your total payment — the majority goes toward interest. As your loan matures and the outstanding balance declines, the proportion going to principal gradually increases.

Interest is the cost of borrowing — the fee your mortgage lender charges for providing the loan capital. It is calculated monthly as a fraction of your outstanding loan balance multiplied by your annual interest rate divided by twelve. In the early months of a mortgage, interest dominates the payment structure.

Property Taxes are assessed by your local government based on the assessed value of your property and the applicable tax rate in your municipality. Most mortgage lenders collect property tax payments monthly as part of your total payment and hold them in an escrow account, disbursing them to the tax authority when they become due. Your monthly property tax contribution is typically one-twelfth of your annual property tax bill.

Homeowner’s Insurance — sometimes called hazard insurance — protects the structure and contents of your home against damage from fire, storms, and other covered events. Like property taxes, homeowner’s insurance premiums are typically collected monthly in escrow and paid annually by the lender on your behalf.

Private Mortgage Insurance — PMI is required on conventional loans where the down payment is less than 20% of the purchase price. PMI protects the lender — not the borrower — against loss in the event of default, and its cost is passed to the borrower as a monthly premium typically ranging from 0.5% to 1.5% of the original loan amount annually. PMI can be cancelled on conventional loans once the borrower reaches 20% equity in the property, either through principal paydown, home value appreciation, or a combination of both.

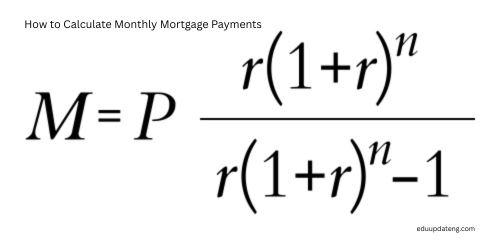

The Core Mortgage Payment Formula

The mathematical foundation of the monthly mortgage payment calculation is the standard fixed-payment loan amortization formula. This formula calculates the fixed monthly payment required to fully repay a loan of a given amount at a given interest rate over a given number of payment periods.

The formula is:

M = P × [r(1 + r)^n] ÷ [(1 + r)^n − 1]

Where:

- M is the monthly principal and interest payment

- P is the principal loan amount — the amount borrowed

- r is the monthly interest rate — the annual interest rate divided by 12

- n is the total number of monthly payments — the loan term in years multiplied by 12

This formula calculates only the principal and interest portion of your monthly payment. Property taxes, homeowner’s insurance, PMI, and HOA fees are added separately to arrive at your total monthly housing payment.

Step-by-Step Mortgage Payment Calculation: A Worked Example

Let us walk through a complete mortgage payment calculation using a realistic example to illustrate exactly how the formula operates in practice.

Scenario: You are purchasing a home with a purchase price of $450,000. You are making a 10% down payment of $45,000, resulting in a loan amount of $405,000. Your mortgage lender has offered you a 30-year fixed rate mortgage at an annual interest rate of 7.25%. Your annual property taxes are $6,000 and your annual homeowner’s insurance premium is $1,800. Your lender requires PMI at a rate of 0.85% of the original loan amount annually.

Step One: Identify Your Variables

- P (loan amount) = $405,000

- Annual interest rate = 7.25%

- r (monthly interest rate) = 7.25% ÷ 12 = 0.604167% = 0.00604167

- Loan term = 30 years

- n (total monthly payments) = 30 × 12 = 360

Step Two: Calculate the Principal and Interest Payment

Applying the formula:

M = $405,000 × [0.00604167 × (1 + 0.00604167)^360] ÷ [(1 + 0.00604167)^360 − 1]

First, calculate (1 + 0.00604167)^360:

(1.00604167)^360 ≈ 8.8497

Now apply the full formula:

M = $405,000 × [0.00604167 × 8.8497] ÷ [8.8497 − 1]

M = $405,000 × [0.053474] ÷ [7.8497]

M = $405,000 × 0.006812

M ≈ $2,759 per month (principal and interest)

Step Three: Add Property Taxes

Annual property taxes of $6,000 ÷ 12 = $500 per month

Step Four: Add Homeowner’s Insurance

Annual premium of $1,800 ÷ 12 = $150 per month

Step Five: Add Private Mortgage Insurance

Annual PMI of 0.85% × $405,000 = $3,442.50 ÷ 12 = $287 per month

Step Six: Calculate Total Monthly Payment

Total monthly payment = $2,759 + $500 + $150 + $287 = $3,696 per month

This figure — $3,696 — is your true monthly housing payment, not simply the $2,759 principal and interest figure that lenders sometimes quote in isolation. Understanding the full PITI plus PMI calculation protects you from budget surprises and gives you an accurate picture of your real monthly housing cost.

How Loan Term Affects Your Monthly Payment

One of the most consequential variables in the monthly mortgage payment calculation is the loan term — the number of years over which you will repay the loan. Comparing payment amounts across different term lengths on the same loan amount and interest rate reveals the fundamental trade-off between monthly affordability and total interest cost.

Using the same $405,000 loan amount at 7.25% annual interest rate from our earlier example:

A 30-year fixed rate mortgage produces a monthly principal and interest payment of approximately $2,759 — the lowest monthly obligation of any standard fixed rate option. However, over 360 payments you will pay approximately $588,000 in total interest, nearly 1.5 times the original loan amount.

A 20-year fixed rate mortgage typically carries a slightly lower interest rate than the 30-year option — assume 6.85% for this comparison. The monthly payment rises to approximately $3,108, but total interest paid drops to approximately $340,000 — a reduction of nearly $248,000 relative to the 30-year option.

A 15-year fixed rate mortgage typically carries the lowest rate of any standard fixed rate option — assume 6.50% for this comparison. The monthly payment increases to approximately $3,529, but total interest paid drops to approximately $230,000 — a reduction of approximately $358,000 relative to the 30-year mortgage.

These comparisons make the trade-off explicit: the 30-year mortgage provides maximum monthly payment affordability at the cost of dramatically higher total interest. The 15-year mortgage minimizes total interest cost but demands a significantly higher monthly payment. The 20-year occupies an intermediate position. The right term choice depends on your specific monthly cash flow requirements, your alternative investment opportunities, your risk tolerance, and your long-term financial planning objectives — a decision best evaluated with the assistance of a certified financial planner.

How Interest Rate Changes Affect Monthly Payments

Interest rate is the single variable with the most dramatic effect on monthly mortgage payment amounts, and understanding its impact quantitatively is essential for both initial mortgage decisions and refinancing analysis.

Using a $400,000 loan amount on a 30-year fixed rate mortgage across different interest rate scenarios:

At 5.00%, the monthly principal and interest payment is approximately $2,147 and total interest paid over 30 years is approximately $373,000.

At 6.00%, the monthly payment rises to approximately $2,398 — an increase of $251 per month — and total interest climbs to approximately $463,000.

At 7.00%, the monthly payment rises to approximately $2,661 — an increase of $514 per month relative to the 5% scenario — and total interest reaches approximately $558,000.

At 7.50%, the monthly payment is approximately $2,797 — an increase of $650 per month relative to 5% — and total interest paid over the life of the loan exceeds $607,000.

At 8.00%, the monthly payment reaches approximately $2,935 and total interest paid exceeds $657,000 — nearly $284,000 more than the same loan at 5%.

These figures illustrate in concrete terms why mortgage rate optimization — through credit score improvement, aggressive lender comparison, strategic discount point evaluation, and intelligent rate lock timing — produces such dramatic lifetime financial impact. Every fraction of a percentage point secured through preparation and negotiation translates into thousands of dollars in savings.

Understanding Mortgage Amortization

Amortization is the process by which your fixed monthly payment is applied first to interest and then to principal reduction over the life of the loan. In the early stages of a mortgage, the majority of each payment goes to interest — leaving very little to reduce the outstanding balance. As the loan matures, the interest component of each payment gradually decreases as the outstanding balance declines, and the principal component correspondingly increases.

This front-loading of interest has several important implications that every mortgage borrower should understand. First, making additional principal payments early in the loan term — even relatively small amounts — produces disproportionately large reductions in total interest paid, because eliminating principal early prevents the accumulation of interest charges on that balance over the remaining term.

Second, refinancing a mortgage resets the amortization schedule from the beginning. A borrower who refinances a 30-year mortgage after ten years of payments into a new 30-year loan effectively extends their total mortgage duration to forty years and restarts the front-loaded interest phase — an important consideration in refinancing analysis that is easy to overlook when focusing solely on the rate reduction.

Third, in the early years of a mortgage, your outstanding loan balance declines very slowly relative to your total payments made — a phenomenon that can produce negative equity risk if property values decline shortly after purchase, particularly for high loan-to-value loans.

A detailed amortization schedule — available through most online mortgage calculators, loan officer tools, spreadsheet applications, and financial planning software — shows the exact principal and interest breakdown of every payment throughout the loan term and tracks the outstanding balance after each payment. Reviewing your amortization schedule in detail provides a complete picture of how your mortgage functions financially over its full life.

Online Mortgage Calculators and Digital Tools

While the mathematical formula for monthly mortgage payment calculation is entirely accessible to any borrower willing to apply it, the practical reality is that most borrowers will use digital tools for routine payment estimation. Understanding which tools are most reliable and what they can and cannot tell you is valuable context for using them effectively.

Most major mortgage lender websites — including Rocket Mortgage, loanDepot, Better.com, and Bankrate — offer free online mortgage payment calculators that allow you to input loan amount, interest rate, loan term, property tax estimates, and insurance costs to produce a complete PITI payment estimate. The Bankrate mortgage calculator and the NerdWallet mortgage calculator are widely regarded as among the most comprehensive free tools available, including PMI estimation, amortization schedule generation, and side-by-side loan comparison functionality.

The Consumer Financial Protection Bureau offers a free mortgage calculator tool on its website that incorporates taxes and insurance estimates alongside the principal and interest calculation, making it a useful and trustworthy resource from a regulatory agency with no commercial interest in influencing your lender selection.

Spreadsheet applications including Microsoft Excel and Google Sheets have built-in PMT functions that calculate monthly loan payments directly — the PMT(rate, nper, pv) function accepts monthly interest rate, number of payments, and present value as inputs and returns the monthly principal and interest payment instantly, making spreadsheet-based analysis a powerful tool for running multiple rate, term, and loan amount scenarios in parallel.

Mortgage amortization schedule generators — available through financial planning software platforms including Quicken, Personal Capital, and YNAB — allow you to model full amortization schedules, analyze extra payment scenarios, and integrate your mortgage payment analysis into a comprehensive household budget and net worth tracking framework.

The Impact of Extra Payments on Your Mortgage

One of the most financially powerful strategies available to any mortgage borrower is the deliberate application of additional principal payments above the required monthly amount. Understanding the mathematical impact of extra payments on your loan balance and total interest cost transforms an abstract principle into a concrete and highly motivating financial strategy.

On a $400,000 loan at 7.00% over 30 years, the standard monthly principal and interest payment is approximately $2,661 and total interest paid over the life of the loan is approximately $558,000.

Adding just $200 per month in additional principal payments — bringing the total payment to approximately $2,861 — reduces the loan payoff to approximately 26 years and reduces total interest paid to approximately $468,000 — a savings of approximately $90,000 in total interest and four years of payments eliminated.

Adding $500 per month in additional principal payments reduces the payoff to approximately 22 years and total interest to approximately $379,000 — a saving of approximately $179,000 and eight years of payments.

These numbers are compelling evidence that even modest additional payment discipline — whether from annual bonuses, tax refunds, regular automatic transfers, or budget optimization — produces enormous long-term financial benefit. Your mortgage lender, certified financial planner, or financial advisor can help you model the optimal extra payment strategy for your specific cash flow, investment alternative opportunities, and long-term financial planning goals.

Calculating Mortgage Payments for Refinancing Scenarios

Understanding the monthly payment calculation is equally valuable when evaluating mortgage refinancing opportunities. A refinance replaces your existing mortgage with a new loan — ideally at a lower interest rate, a different term, or both — and calculating the new payment alongside the break-even analysis determines whether the refinance produces genuine financial benefit.

The break-even calculation compares the monthly payment savings produced by the rate reduction against the total closing costs of the refinance transaction. Dividing total closing costs by monthly savings produces the break-even period in months — the point at which cumulative savings equal the upfront cost. If you plan to remain in the home and maintain the mortgage for longer than the break-even period, the refinance produces net financial benefit.

For example, refinancing a $350,000 remaining balance from 7.50% to 6.75% on a new 30-year term reduces the monthly principal and interest payment from approximately $2,447 to approximately $2,270 — a monthly saving of approximately $177. If the total closing costs of the refinance are $8,500, the break-even period is approximately 48 months — four years. If you plan to stay in the home for more than four years, the refinance makes financial sense. If your planned holding period is shorter, the upfront cost exceeds the recoverable benefit.

A cash-out refinance replaces your mortgage with a larger loan, accessing accumulated home equity for purposes such as home improvement financing, debt consolidation, investment funding, or education costs. The new monthly payment calculation incorporates the higher loan balance alongside the prevailing rate and term, and the financial analysis must weigh the payment increase and additional interest cost against the value and return of the use to which the extracted equity is put.

Working with a certified financial planner and an independent mortgage advisor when evaluating refinancing decisions ensures that the analysis is comprehensive — accounting for opportunity cost, tax implications of mortgage interest, private mortgage insurance changes, and the interaction of the refinance decision with your overall investment and retirement planning strategy.

Property Tax and Insurance Escrow: What Gets Added to Your Payment

Property taxes and homeowner’s insurance are collected by most mortgage lenders on a monthly basis through an escrow account — a separately held account that the lender manages and from which tax and insurance payments are disbursed to the relevant authorities and insurance carriers when due.

Your monthly escrow contribution is calculated by the lender based on the most recent property tax assessment and your current homeowner’s insurance premium, divided by twelve, with a small cushion — typically two months of escrow payments — maintained as a reserve against future increases. Your escrow account is reviewed annually — typically through an escrow analysis — and your monthly contribution is adjusted upward or downward if the actual tax or insurance costs have changed relative to the projected amounts.

Property tax rates vary enormously by municipality. In high-tax states such as New Jersey, Illinois, and Connecticut, annual property taxes can represent 2% to 3% or more of the property’s assessed value — adding several hundred dollars per month to the total mortgage payment on a mid-price home. In lower-tax states such as Hawaii, Alabama, and Colorado, annual property taxes can be well below 0.5% of assessed value, adding a much more modest monthly amount.

Flood insurance, earthquake insurance, and windstorm insurance — required in certain high-risk geographic areas as a condition of mortgage approval — can add meaningfully to monthly housing costs beyond the standard homeowner’s insurance premium and should be accounted for in full payment calculations when purchasing in designated hazard zones.

Frequently Asked Questions

How do I calculate my exact monthly mortgage payment? Use the formula M = P × [r(1 + r)^n] ÷ [(1 + r)^n − 1] where P is your loan amount, r is your monthly interest rate (annual rate divided by 12), and n is your total number of payments (years × 12). Then add property taxes, homeowner’s insurance, and PMI if applicable.

What is included in a monthly mortgage payment? A complete monthly mortgage payment typically includes principal, interest, property taxes collected in escrow, homeowner’s insurance collected in escrow, and private mortgage insurance if your down payment was less than 20%.

Does my monthly mortgage payment change over time on a fixed rate loan? The principal and interest portion of your payment remains constant on a fixed rate mortgage. However, your escrow component — property taxes and insurance — may change annually as tax assessments and insurance premiums fluctuate, causing modest changes to your total monthly payment.

How does making extra payments affect my mortgage? Additional principal payments reduce your outstanding loan balance faster, shorten your loan payoff timeline, and reduce the total interest paid over the life of the loan — often dramatically. Even modest consistent extra payments produce significant long-term savings.

What is an amortization schedule? An amortization schedule is a complete table showing the breakdown of every monthly mortgage payment into principal and interest components throughout the entire loan term, along with the outstanding balance after each payment.

How do I know if refinancing will reduce my monthly payment enough to be worth it? Calculate your new monthly payment at the proposed rate and term, subtract it from your current payment to find the monthly saving, then divide your total closing costs by that saving to determine the break-even period in months. If your anticipated remaining holding period exceeds the break-even period, refinancing produces net financial benefit.

Conclusion: Payment Calculation Knowledge Is Financial Power

The ability to calculate, understand, and strategically manage your monthly mortgage payment is not a specialized skill reserved for financial professionals — it is practical financial literacy that every homebuyer, homeowner, and real estate investor should possess. When you understand exactly how your payment is derived, you can compare lenders with genuine confidence, evaluate refinancing opportunities with mathematical precision, plan your household budget with complete accuracy, and make additional payment decisions with clear knowledge of their financial impact.

Read Also: Best Mortgage Lenders for First-Time Buyers in 2026: The Complete Comparison Guide

Armed with the formula, the worked examples, the amortization understanding, and the digital tools in this guide, you have everything you need to approach every mortgage payment decision — whether buying your first home, refinancing an existing loan, accessing home equity, or investing in property — with the financial intelligence and analytical confidence of a genuinely informed borrower.

Work with a certified financial planner, a licensed mortgage advisor, and a reputable mortgage lender or independent mortgage broker to translate this understanding into optimal real-world mortgage decisions for your specific financial situation. The numbers are knowable, the tools are accessible, and the financial rewards of payment calculation mastery are real and lasting.

Share the article with others if you find it helpful.

Conversation

0 Comments